Introduction

In this section of Next Mile M&A’s primary content category – Exit Readiness and Planning – we’ll explore key considerations in determining if your transportation business is ready to sell.

Exit Motivation

Reasons to Exit

There can be many motivational reasons for the desire to exit a business. Here are just a few:

- Age

- Health considerations

- Financial reward

- Transportation ownership fatigue

- Lifestyle improvement

Timing

Most transportation acquisition deal structures contain an earnout provision for a Seller to obtain the full deal valuation. There are literally hundreds of deal structure variations within two primary categories:

- 100% purchase

- Buyer applies a multiple to the trailing 12-month (TTM or LTM) period normalized (expenses credited for anomalies that won’t continue forward) earnings based on many different factors, pays a percentage of that in upfront cash, and the remaining over a designated period (typically known as earnout) with an earnings baseline requirement. Earnout timelines typically stretch from 1 to 3 years and Sellers are typically required to remain in the business by Buyers during earnout. Most Sellers want to remain in the business during earnout to control their destiny as it pertains to realizing the deal full valuation.

- Equity retainment

- Seller retains equity for what is referred to as having the ability to, “Take a second bite of the apple.” Both Buyer and Seller share in the rewards of future growth and profitability over a timeframe that is typically much greater than earnout.

- Due diligence

- Along with the timeline it takes to compile the Seller’s initial data, introduce multiple Buyers (NEVER consider one Buyer), and finalize the Letter of Intent (LOI or IOI) details, a Introduction Seller must navigate a lengthy due diligence period that can extend beyond 6 months. It is very common for Sellers to experience what is known in the industry as “Seller fatigue” during the due diligence process. Next Mile M&A can significantly reduce timelines with its proprietary software – Acquisitions Powered by Code© – which automates the acquisition process and generates virtually every analytic a Buyer will want to see deep in the due diligence process, at the start of the acquisition process. This technological advantage over all other M&A firms is deeply engrained in many of the Next Mile M&A articles.

This topic of Timing is covered in greater detail within the Next Mile M&A’s “How Long Does It

Really Take to Sell a Logistics Business?” and “Understanding Deal Structures”

Financial Considerations

Sellers often struggle with the correct time to sell. There are so many variables that can affect a transportation business, and many of them are not within control of the seller. Market capacity, political direction, the U.S. overall economy, existing customer instability, are just a few factors that a Seller has little control over. Next Mile M&A has worked with many Sellers that have opted out of selling in hopes of what were relatively few upside dollars, only to end up selling their business for less. This is why Next Mile M&A has always advised prospective Sellers to consider an acquisition trigger point that will provide a financial legacy for their immediate family, and potentially the next generation. If a Seller can garner enough to financially set a family for at least the seller’s expected lifespan, the Seller should seriously consider if it is worth gambling in hopes for some additional financial consideration.

Financial Readiness

Financial Accuracy

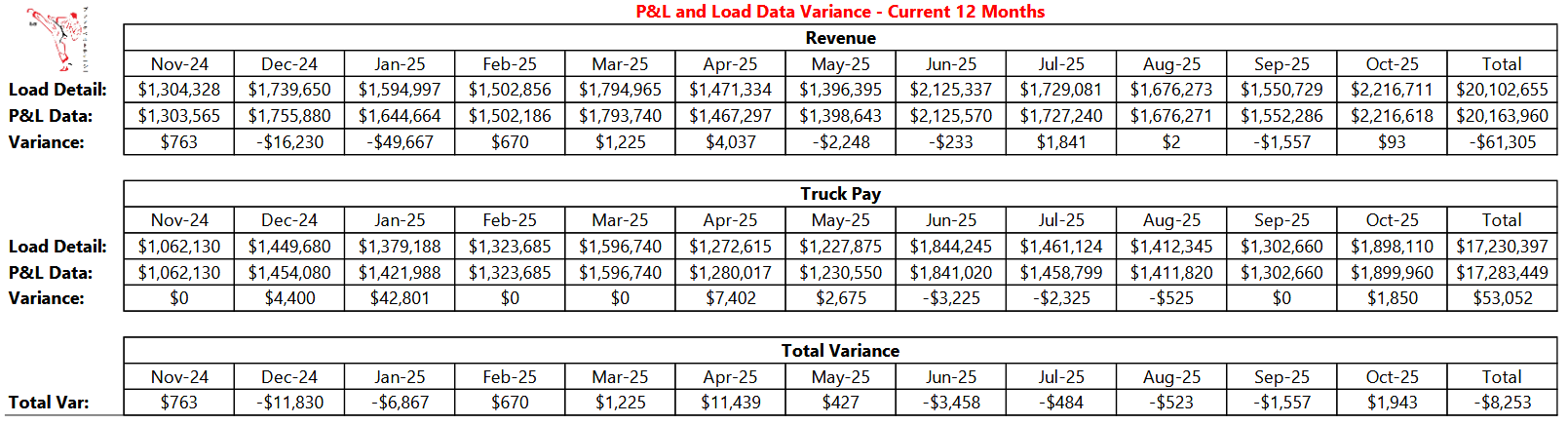

One of the most significant mistakes a business can make is to go to market only to have a Buyer find financial errors. This automatically creates distrust with the Buyer and can destroy an exit strategy for an extended period. Most prospective Sellers are very confident in their accounting firm and the numbers provided. The Black Belt TC proprietary technology – Acquisitions Powered by Code© – can upload financial data from any financial management system and load data from any TMS. Along with generating advanced business analytics it also runs comparisons of financial and load data to find errors at the start of the acquisition process, prior to taking a Seller to market. Since its inception this system has documented finding more than $1.75m of EBITDA calculation errors. Each business had an accounting firm it relied on for accurate financial statements. The chart below depicts a comparison of financial statement data against the load data of a Seller. It is just one example of cross-referencing the Next Mile M&A proprietary software performs regularly to capture financial irregularities. Other M&A firms do not even ask for load data since they don’t have a way to process it and TMS platforms

typically do not house financial data to run comparisons and checks. It is further complicated by the fact that some line items in the financial Revenue (Income) and Cost of Goods Sold (Direct Cost) may not flow into the load data.

Types of Data Buyers Want to See

The problem with most data generated from financial management systems and TMS is that many of the details Buyers want to review are not readily available, or it takes a Buyer substantial time to garner the data in the desired format. This will quite often lengthen the process or eventually cause a deal to be re-traded during due diligence. Re-trading is an acquisition term used when an original valuation is lowered by a Buyer after financial irregularities, or additional risk factors are discovered that were not previously known. Next Mile M&A categorizes the primary data types into two main categories:

Valuation Drivers

(more impact on the multiple)

- Revenue trends across the last three full fiscal years, current year, and TTM period

- Gross profit trends across the last three full fiscal years, current year, and TTM period

- Gross profit by mode – provides a Buyer with market comparisons on profitability by mode

- EBITDA trends across the last three full fiscal years, current year, and TTM period

- Normalized expense calculations with detailed descriptions for the last three full fiscal years, current year, and each month within the TTM period

- These expense add-backs can be critical to a Buyer’s valuation and come under heavy scrutiny, especially if a Seller is not familiar with the intricacies of which line items and the proper amounts to claim.

- Line item and normalized EBITDA percentage of revenue trends across the last three full fiscal years, current year, and TTM period

- Seller culture, personalities, skillsets, and strategic fit within a Buyer

Risk Factors

(more impact on the deal structure – % cash at close & earnout duration)

- Revenue concentration

- Gross profit concentration

- Mode concentration

- Commodity concentration

- Industry concentration

- Lane concentration

- DSO and bad debt history

- Mitigating factors

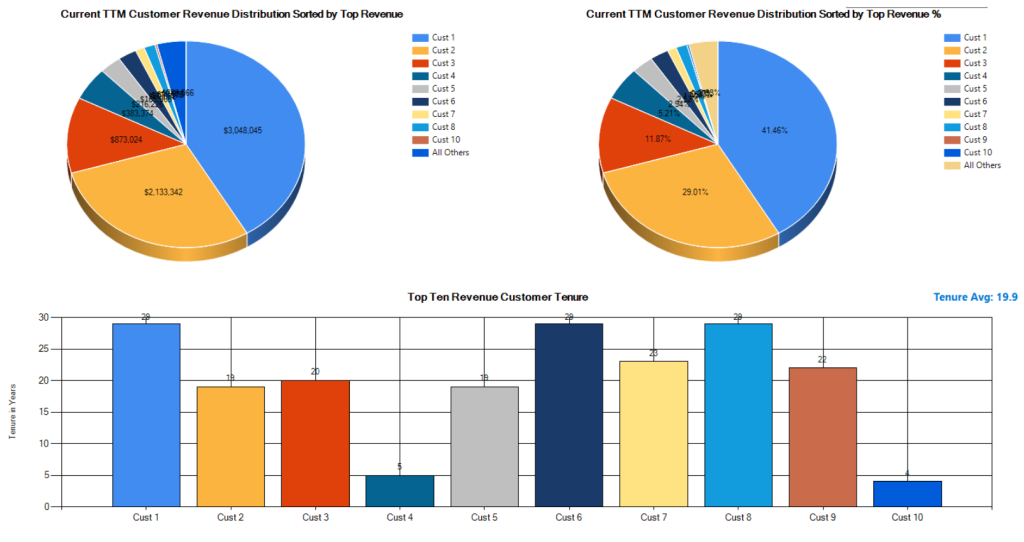

- These factors can assist in limiting perceived Buyer risk. Here is one example of revenue concentration that is somewhat mitigated with extremely strong customer tenure

Financial Data Consolidation

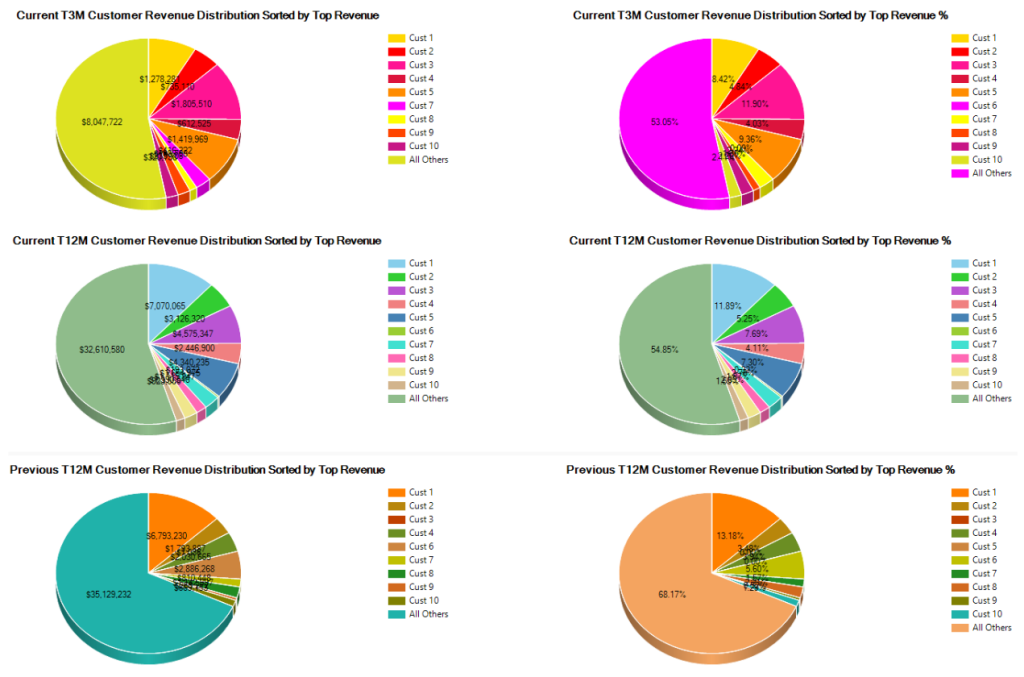

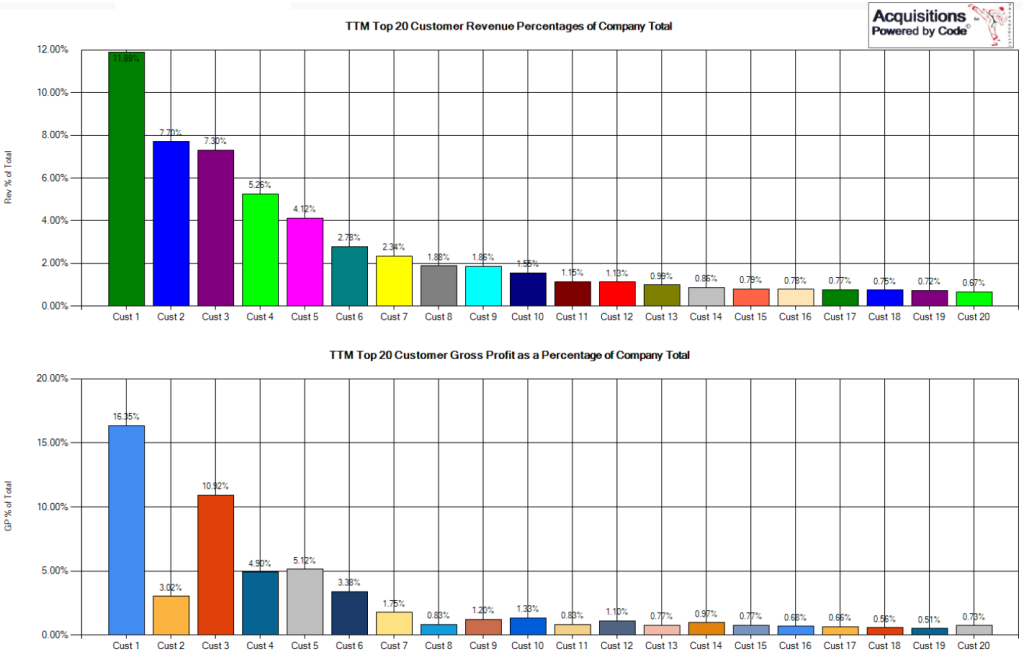

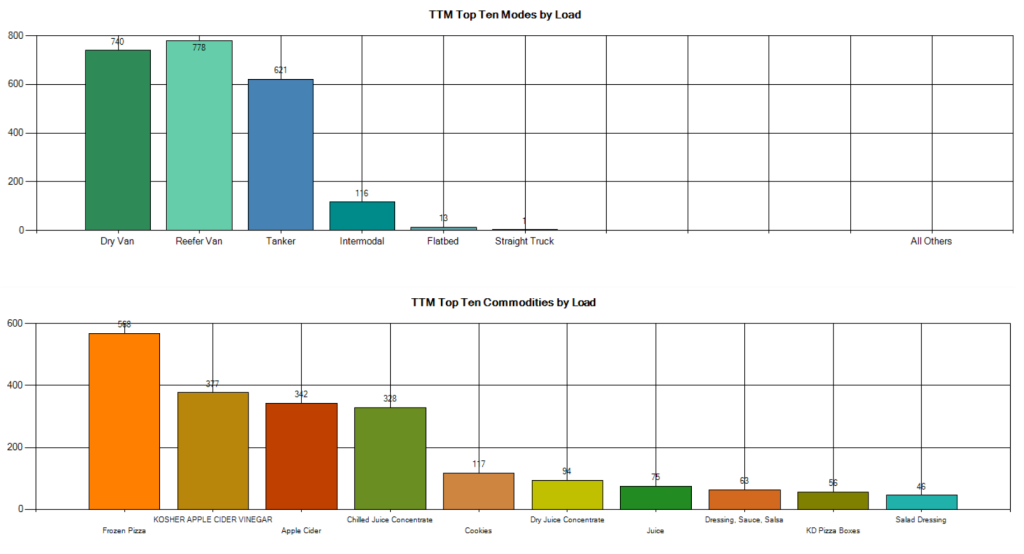

When data is consolidated and all positive and negative aspects of a Seller are openly displayed early in the process, the acquisition timeline is cut short, and the Seller will be more likely to benefit with more positive valuations and deal structure offers. Next Mile M&A’s proprietary technology is specifically designed with this in mind. The system generates over 430 graphs and charts that provide data that many TMS’ either cannot generate or require a Buyer to piece together multiple reports to extract the data desired. Here are two reports generated by Acquisitions Powered by Code© that literally took 18 pages of reporting from a TMS to provide the same data covering the same timeframe.

(2nd report on the following page)

It is important to note that naming convention issues in TMS’ can be problematic and misleading for Buyers. For example, entries in a TMS may be made for a particular customer name, along with the location within the name. This may be misleading for a Buyer that early in the process counts the total number of customers to determine revenue concentration when the actual number of customers may be significantly less. This could cause a deal valuation and structure to be re-traded in due diligence when greater scrutiny is taken while examining the data. Other common examples include the inability for a TMS to generate accurate top ten mode data since there can be so many descriptions of a dry van alone. Commodity data is a risk factor that few TMS’ can generate. An example would be a transportation company heavy in building material commodities. Obviously, there is more risk in an economic downturn that a Seller heavily concentrated in foodstuff. The Next Mile M&A system can correct all these issues at the start of the acquisition timeline, and keep it consistent throughout the entire process, so the data is meaningful and precise for a Buyer.

(two examples on the following page)

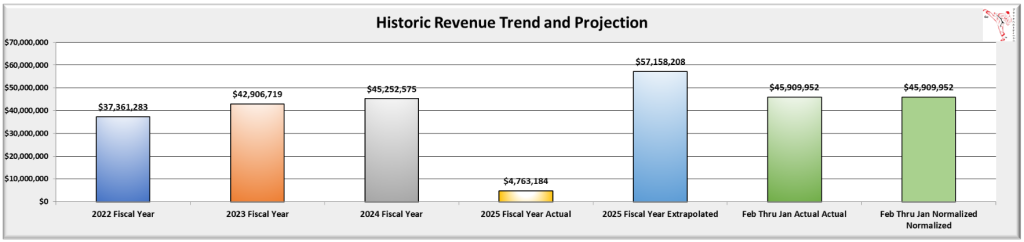

Business Trends and Projections

A Seller should also have accurate projections supported by factual data prior to going to market. If a Seller’s current trend and extrapolated data is down and future projections are unreasonably high the data will obviously receive a lot of scrutiny from a Buyer and may potentially create a negative trust factor between Seller and Buyer. The data needs to be clear and concise with factual support.

Business Trends and Projections

These are two categories that may affect a Buyer’s desire to make an offer on a business or severely impact the deal structure with a Buyer requiring unusually high escrows or more restrictive stipulations within the earnout language. The level of severity and timelines can play an important role in determining the correct timing for a Seller to go to market.

Key Takeaways

- Reason for exit can be an important consideration for strategic Buyers

- Timing on going to market will be impacted by the type of deal structure desired. There are many structures that provide benefit for growth during earnout periods so Sellers don’t need to wait for what may be the ultimate moment to sell.

- Sellers should consider an acquisition trigger point that will provide a financial legacy for their immediate family, and potentially the next generation.

- The most significant mistake a Seller can make is to only consider one Buyer

- The acquisition process can be lengthy, exhaustive, and complex which is why Sellers should seek professional help in navigating all the complexities to find the Best Value Buyer

- Financial accuracy is critical and many Sellers lose value in not properly normalizing expenses

- Data consolidation and accuracy are critical to maximize value and prevent deal re-trading late in the acquisition process.

- Focus on the Valuation Drivers and Risk Factors and make certain that a selected M&A firm can accurately generate all this data upfront in the process

- Make certain that business projections are clear and concise with facts and not random numbers that are “pie in the sky”

- Legal and safety issues should be considered based on the degree of severity and timelines relative to when a Seller goes to market